Matthew Emery, CFA, is responsible for analyzing companies in the retail industry. He is currently reviewing the status of Ferguson Department Stores, Inc. (FDS). FDS has recently gone through extensive restructuring in the wake of a slowdown in the economy that has made retailing particularly challenging. As part of his analysis, Emery has gathered information from a number of sources.

Ferguson Department Stores, Inc.

FDS went public in 1969 following a major acquisition, and the Ferguson name quickly became one of the most recognized in retailing. Ferguson had been successful through most of its first 30 years in business and has prided itself on being the one-stop shopping destination for consumers living on the West Coast of the United States. Recently, FDS began to experience both top and bottom line difficulties due to increased competition from specialty retailers who could operate more efficiently and offer a wider range of products in a focused retailing sector. When the company's main bank reduced FDS's line of credit, a serious working capital crisis ensued, and the company was forced to issue additional equity in an effort to overcome the problem. FDS has a cost of capital of 10% and a required rate of return on equity of 12%. Dividends are growing at a rate of 8%, but the growth rate is expected to decline linearly over the next six years to a long-term growth rate of 4%. The company recently paid an annual dividend of $1.

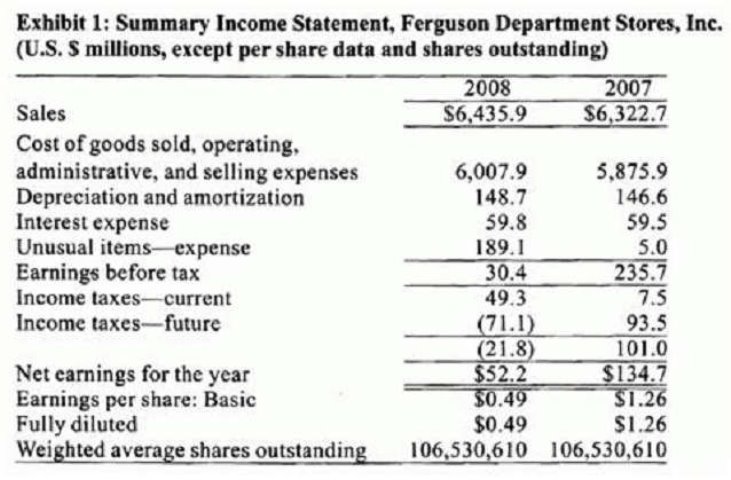

At the end of 2008, FDS announced that it would be expanding its retail operations, moving to a warehouse concept, and opening new stores around the country. FDS also announced it would close some existing stores, write-down assets, and take a large restructuring charge. Upon reviewing the prospects of the firm, Emery issued an earnings per share forecast for 2009 of $0.90. He set a 12-month share price target of $22.50. Immediately following the expansion announcement, the share price of FDS jumped from $14 to $18.

In 2008, FDS also reported an unusual expense of $189.1 million related to restructuring costs and asset write downs.

In response to questions from a colleague, Emery makes the following statements regarding the merits of earnings yield compared to the P/E ratio:

Statement 1: For ranking purposes, earnings yield may be useful whenever earnings are either negative or close to zero.

Statement 2: A high E/P implies the security is overpriced.

Given Emery's dividend forecast for FDS, is the H-model the appropriate valuation model to use to value FDS?

Select an option, then click Submit answer.

-

○

Yes.

-

○

No, the H-model is appropriate when the dividend growth rate declines at a linear rate for a short period of time during stage one, followed by a 1 -year suspension in dividends before the previous dividend is reinstated, and then dividends grow at a long-term constant rate.

-

○

No, the H-model is appropriate when the dividend growth rate grows during the first stage followed by a period of stable growth in dividends in stage two, followed by a dividend growth rate that declines linearly in perpetuity.