Austin Clark, CFA, has been asked to analyze White Goods Corporation, a $9 billion company that owns a nationwide chain of stores selling appliances and other electronic goods. As part of his analysis of the White Goods Corporation, Clark's supervisor, David Horvath, asks Clark to forecast White Goods' 2009 sales using multiple regression analysis. The following model was developed:

sales = 20.1 + 0.001 GDP+ 1,000.6 TR + 0.1 CC -3.2 PC -40.3 UR t-values: (1.1) (2.3) (1.75) (3.2) (-0.48) (-0.9)

Number of observations: 76

Standard error estimate: 15.67

Unadjusted R2: 0.96

Regression sum of squares: 412,522 Error sum of squares: 17,188

Independent Variable Descriptions

GDP = gross domestic product

TR = average coupon rate on 5-year U.S. Treasury securities

CC = most recent quarter end consumer confidence index value

PC = previous year's sales of personal computers UR = most recent quarter end unemployment rate

Variable Estimates for 2009

GDP =8,000

TR = 0.05

CC =97

PC = 60,000

UR = 0.055

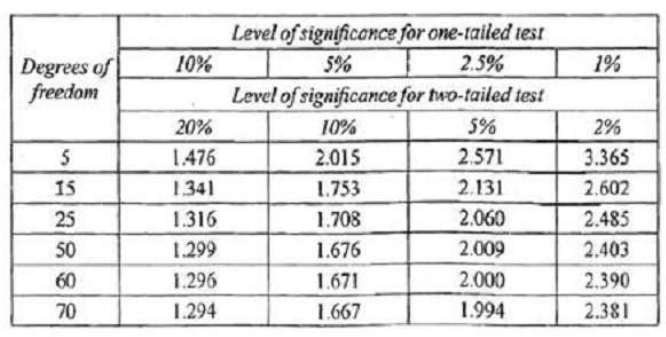

Critical Values For Student's t-Distribution

Clark's supervisor asks him to prepare a report explaining the implications of the regression analysis results. Clark writes the following conclusions concerning regression analysis in his report:

Interpreting the results of regression analysis can be problematic if certain assumptions of the ordinary least squares framework are violated. The regression output for White Goods Corporation is unreliable for the following reasons:

Finding 1: The correlation between regression errors across time is very close to 1.

Finding 2: There is a strong relationship between the regression error variance and the regression independent variables.

Is the regression coefficient of the 5-year U.S. Treasury interest rate statistically significantly different from zero at the 10% level of significance?

Select an option, then click Submit answer.

-

○

Yes, because 1.75 > 1.29.

-

○

Yes, because 1.75 > 1.67.

-

○

No, because 1.75 < 1.99.

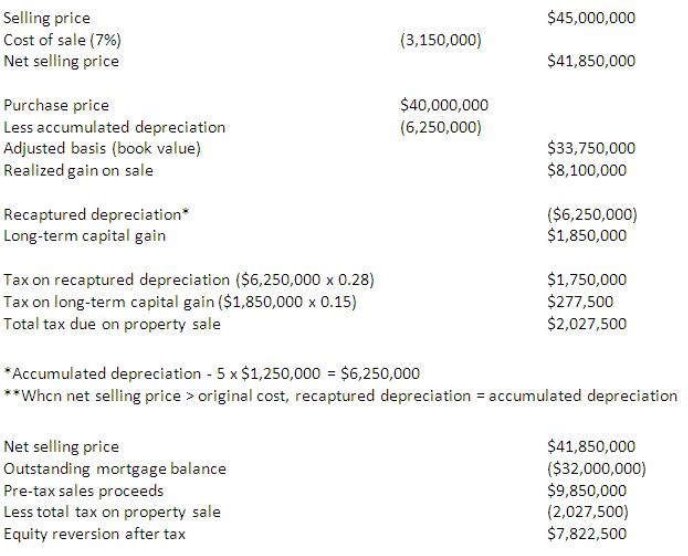

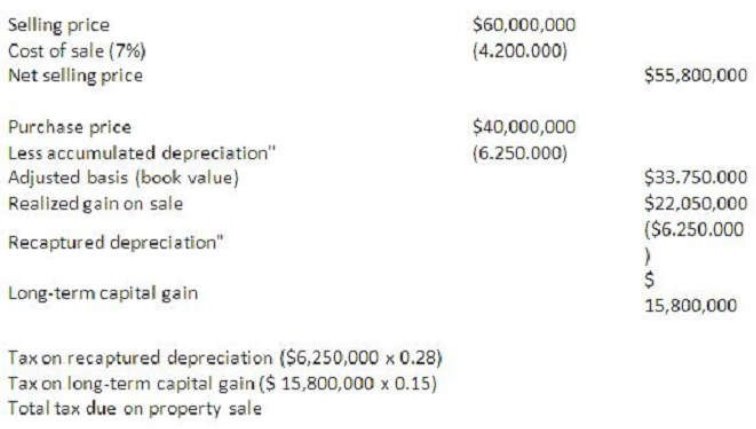

At Sentry's request, Larson will evaluate the investment in Riviera Terrace over a 5-year horizon using selling prices of $45,000,000 and S60,000,000.

At Sentry's request, Larson will evaluate the investment in Riviera Terrace over a 5-year horizon using selling prices of $45,000,000 and S60,000,000.