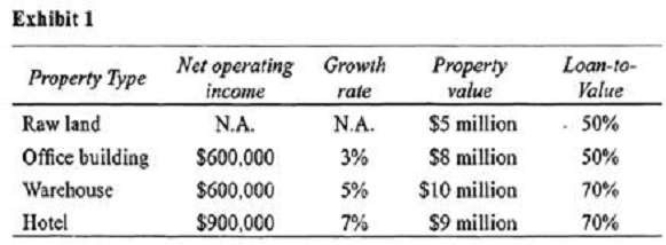

Josh Atwell recently inherited a large sum of money and wants to invest a portion of the inheritance into a real estate investment that provides a tax shelter. Atwell wants to take a limited management role in the real estate investment, and avoid the expense of hiring professional project management. Also, Atwell requires that the real estate investment generate high cash flows. Atwell hired Kellogg Investments to provide him potential real estate investments. Kellogg created Exhibit 1 outlining alternative real estate investments, from which Atwell can make his selection. Atwell's cost for any loan is 8%. The loan would be amortized over 20 years with annual payments. His required rate of return is 11%.

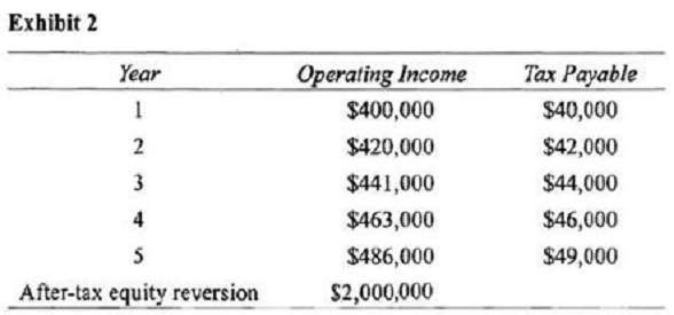

After reviewing the potential real estate investments generated by Kellogg, Atwell decided against all of the choices. Instead, Atwell requested a detailed report on the investment merits of an apartment complex. In Exhibit 2, Kellogg details the operating income of a targeted apartment complex investment. Atwell will make an equity contribution of $1,000,000. The loan-to-value ratio for the apartment complex investment would be 75%.

An adviser from Kellogg states that Atwell should purchase the apartment complex because the net present value of the investment is positive. The adviser also states, however, that the investment's IRR is less than Atwell’s required rate of return. After reviewing the historical financial statements of the potential hotel investment, the advisor notes its erratic net operating income. In fact, the hotel generated several years of growing cash flow followed by two negative years and then a return back to a positive cash flow.

Based on the historical financial statements of the hotel, which of the following valuation techniques would be most appropriate?

Select an option, then click Submit answer.

-

○

The internal rate of return (1RR) approach

-

○

The direct capitalization approach.

-

○

The net present value (NPV) approach.