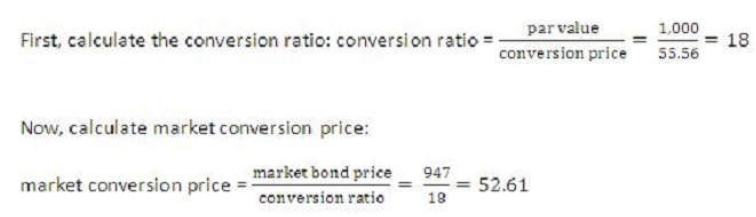

MediSoft Inc. develops and distributes high-tech medical software used in hospitals and clinics across the United States and Canada. The firm's software provides an integrated solution to monitoring, analyzing, and managing output from a variety of diagnostic medical equipment including MRls, CT scans, and EKG machines. MediSoft has grown rapidly since its inception ten years ago, averaging 25% growth in sales over the last decade. The company went public three years ago. Twelve months after their IPO, MediSoft made two semiannual coupon bond offerings, the first of which was a convertible bond. At the time of issuance, the convertible bond had a coupon rate of 7.25%, par value of $1,000, a conversion price of $55.56, and ten years until maturity. Two years after issuance, the bond became callable at 102% of par value. Soon after the issuance of the convertible bond, the company issued another series of bonds which were putable, but contained no conversion or call features. The putable bonds were issued with a coupon of 8.0%, par value of $1,000, and 15 years until maturity. One year after their issuance, the put feature of the putable bonds became active, allowing the bonds to be put at a price of 95% of par value, and increasing linearly over five years to 100% of par value. MediSoft's convertible bonds are now trading in the market for a price of $947 with an estimated straight value of $917. The company's putable bonds are trading at a price of $1,052. Volatility in the price of MediSoft's common stock has been relatively high over the last few months. Currently the stock is priced at $50 on the New York Stock Exchange and is expected to continue its annual dividend in the amount of $1.80 per share.

MediSoft Inc. develops and distributes high-tech medical software used in hospitals and clinics across the United States and Canada. The firm's software provides an integrated solution to monitoring, analyzing, and managing output from a variety of diagnostic medical equipment including MRls, CT scans, and EKG machines. MediSoft has grown rapidly since its inception ten years ago, averaging 25% growth in sales over the last decade. The company went public three years ago. Twelve months after their IPO, MediSoft made two semiannual coupon bond offerings, the first of which was a convertible bond. At the time of issuance, the convertible bond had a coupon rate of 7.25%, par value of $1,000, a conversion price of $55.56, and ten years until maturity. Two years after issuance, the bond became callable at 102% of par value. Soon after the issuance of the convertible bond, the company issued another series of bonds which were putable, but contained no conversion or call features. The putable bonds were issued with a coupon of 8.0%, par value of $1,000, and 15 years until maturity. One year after their issuance, the put feature of the putable bonds became active, allowing the bonds to be put at a price of 95% of par value, and increasing linearly over five years to 100% of par value. MediSoft's convertible bonds are now trading in the market for a price of $947 with an estimated straight value of $917. The company's putable bonds are trading at a price of $1,052. Volatility in the price of MediSoft's common stock has been relatively high over the last few months. Currently the stock is priced at $50 on the New York Stock Exchange and is expected to continue its annual dividend in the amount of $1.80 per share.

High-tech industry analysts for Brown & Associates, a money management firm specializing in fixed-income investments, have been closely following MediSoft ever since it went public three years ago. In general, portfolio managers at Brown & Associates do not participate in initial offerings of debt investments, preferring instead to see how the issue trades before considering taking a position in the issue. Since MediSoft's bonds have had ample time to trade in the marketplace, analysts and portfolio managers have taken an interest in the company's bonds. At a meeting to discuss the merits of MediSofVs bonds, the following comments were made by various portfolio managers and analysts at Brown & Associates:

"Choosing to invest in MediSoft's convertible bond would benefit our portfolios in many ways, but the primary benefit is the limited downside risk associated with the bond. Since the straight value will provide a floor for the value of the convertible bond, downside risk is limited to the difference between the market price of the bond and the straight value."

"Decreasing volatility in the price of MediSoft's common stock as well as increasing volatility in the level of interest rates are expected in the near future. The combined effects of these changes in volatility will be a decrease in the price of MediSoft's putable bonds and an increase in the price of the convertible bonds. Therefore, only the convertible bonds would be a suitable purchase."

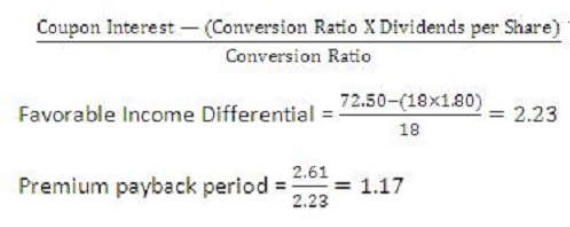

Assuming that portfolio managers at Brown & Associates purchased the convertible bonds, how many years would it take to recover the premium per share?

Select an option, then click Submit answer.

-

○

1.17.

-

○

1.32.

-

○

2.26.