International Opportunity Investors (IOI) manages substantial euro-priced equity portfolios for two

U.S.-based investors, Mark Taylor and Cindy Amsler. Taylor and Amsler have invested in European stocks because of recent media reports suggesting that, due to continued interest rate increases in the United States, European stocks will outperform U.S. stocks over the next few years. Their portfolios are well diversified and similar to the local index portfolio in capitalization weightings.

Ted Tavinsky, lOI's portfolio manager asks his assistant, Tim Treblehorn, to review the relationship between international asset returns and the level of currency risk assumed when investing in foreign securities. The findings, Tavinsky believes, will prove useful in marketing the fund to North American investors. Treblehorn relays two fundamental conclusions to Taylor. First, correlations between international markets have been increasing, and the result has been reduced diversification benefits for international investors. Second, currency risk is typically less than half that of foreign stock risk, but the actual risk assumed is much lower because currency returns and stock returns are not perfectly positively correlated.

Taylor however is very concerned that the U.S. downturn may spread to the global economy. He states that he would like to explore the possibility of investing in the RRIC countries (Brazil, Russia, India, and China). Tavinsky replies that the prospects for the BRIC countries are quite good. Relative to the current G6 countries (U.S., Japan, U.K., Germany, France, and Italy), the stronger economic growth for emerging markets should result in higher stock returns.

Furthermore, the increased growth in these markets will increase the demand for capital, which should strengthen their currency values.

Amsler is a novice investor and has hesitantly invested in the overseas markets. In order to calm her fears, Tavinsky and Treblehorn investigate the possibility of hedging using futures contracts on an equity index as well as a euro forward contract. They have chosen futures contracts written on the Eurostoxx equity index for her portfolio because the price changes of the contract have a high correlation with the returns on Amsler's equity portfolio. Amsler's equity portfolio has a market value of €15,000,000 and a beta of 1.15 relative to the local underlying index.

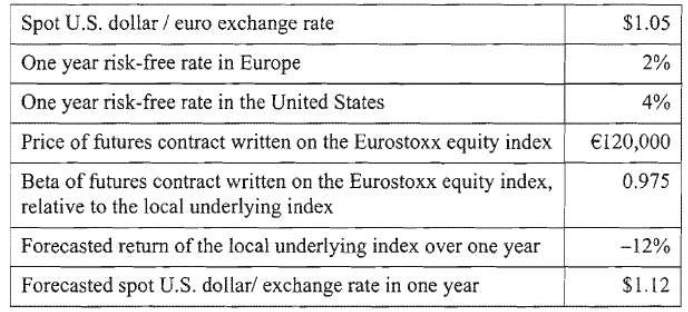

Tavinsky and Treblehorn collect data for spot exchange rates, futures contract prices and betas, as well as U.S. and European interest rates. Tavinsky and Treblehorn are bearish on the European stock market over the next year as noted by their forecasted return for it.

Tavinsky has told Amsler that he and Treblehom will calculate the value of her portfolio in hedged and unhedged scenarios. Tavinsky states that if, at the beginning of the year, he were to fully hedge the systematic risk of Amsler's equity portfolio using the index futures, the appropriate futures position to accomplish this would be 125 contracts. Treblehorn states that if they decide to hedge the currency risk of the portfolio as well, the principal for the forward contract that will hedge the currency risk of the hedged equity position will be €15,000,000, using a ''hedging the principal" strategy.

Lastly, Tavinsky and Treblehorn calculate the forecasted return on the portfolio assuming that currency risk is hedged. Assuming that both equity and currency risk are hedged, Tavinsky calculates that the dollar return would be 8.8%. Treblehorn states that the forecasted spot U.S. dollar / euro exchange rate in one year of $1.12 should be used for the forward contract rate.

Assuming a futures position based on the expected exchange rate in one year turns out to be a perfect hedge and the currency risk is not hedged, the dollar return on the Amsler equity portfolio is closest to:

Select an option, then click Submit answer.

-

○

a 9% gain.

-

○

an 11% gain.

-

○

a 7% loss.