Smiler Industries is a U.S. manufacturer of machine tools and other capital goods. Dat Ng, the CFO of Smiler, feels strongly that Smiler has a competitive advantage in its risk management practices. With this in mind, Ng hedges many of the risks associated with Smiler's financial transactions, which include those of a financial subsidiary. Ng's knowledge of derivatives is extensive, and he often uses them for hedging and in managing Srniler's considerable investment portfolio.

Smiler has recently completed a sale to Frexa in Italy, and the receivable is denominated in euros. The receivable is €10 million to be received in 90 days. Srniler's bank provides the following information:

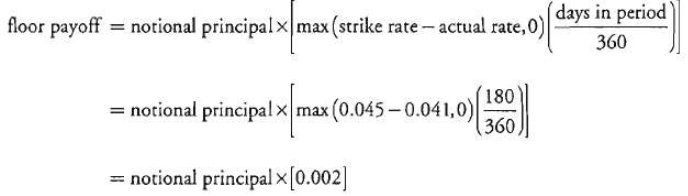

Smiler borrows short-term funds to meet expenses on a temporary basis and typically makes semiannual interest payments based on 180-day LIBOR plus a spread of 150 bp. Smiler will need to borrow S25 million in 90 days to invest in new equipment. To hedge the interest rate risk on the loan, Ng is considering the purchase of a call option on 180-day LIBOR with a term to expiration of 90 days, an exercise rate of 4.8%, and a premium of 0.000943443 of the loan amount. Current 90day LIBOR is 4.8%.

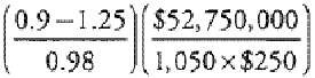

Smiler also has a diversified portfolio of large cap stocks with a current value of $52,750,000, and Ng wants to lower the beta of the portfolio from its current level of 1.25 to 0.9 using S&P 500 futures which have a multiplier of 250. The S&P 500 is currently 1,050, and the futures contract exhibits a beta of 0.98 to the underlying.

Because Ng intends to replace the short-term LIBOR-based loan with long-term financing, he wants to hedge the risk of a 50 bp change in the market rate of the 20-year bond Smiler will issue in 270 days. The current spread to Treasuries for Smiler's corporate debt is 2.4%. He will use a 270-day, 20-year Treasury bond futures contract ($100,000 face value) currently priced at 108.5 for the hedge. The CTD bond for the contract has a conversion factor of 1.259 and a dollar duration of $6,932.53. The corporate bond, if issued today, would have an effective duration of 9.94 and has an expected effective duration at issuance of 9.90 based on a constant spread assumption. A regression of the YTM of 20-year corporate bonds with a rating the same as Smiler's on the YTM of the CTD bond yields a beta of 1.05.

What position should Smiler take to alter the beta of the equity portfolio?

Select an option, then click Submit answer.

-

○

Long 72 futures contracts.

-

○

Short 72 futures contracts.

-

○

Long 70 futures contracts.

which in numeric terms is:

which in numeric terms is: = -71.77; short 72 contracts.

= -71.77; short 72 contracts.